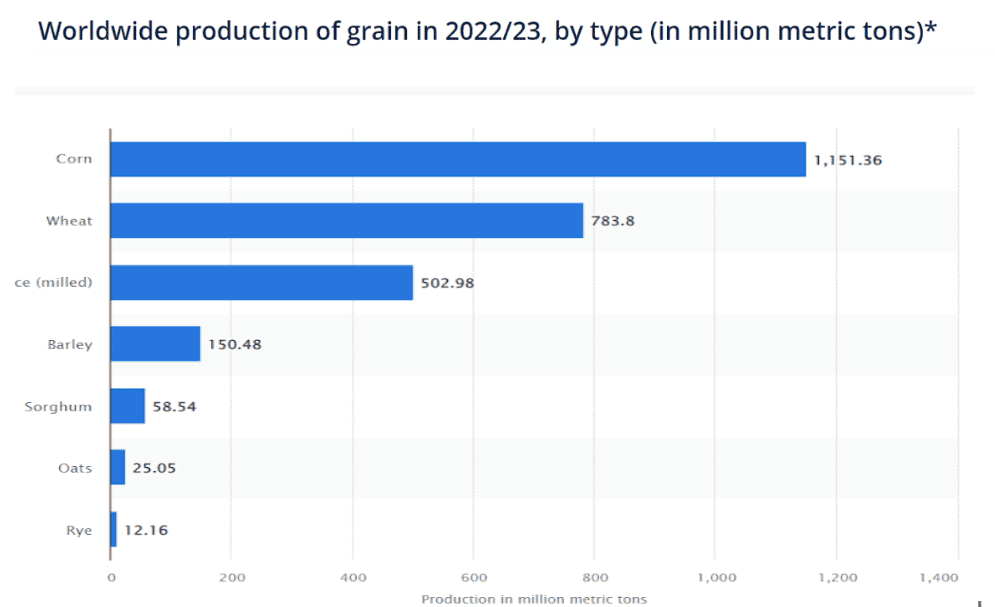

American grain farmers increased their output in response to the growing demand for their products abroad. According to information from the USDA’s National Agricultural Statistics Service's (NASS), Annual Crop Output Report, wheat output marginally decreased while corn, soybeans, and sorghum all enjoyed record-breaking years. According to the same USDA NASS crop report, growers had planted millions more acres of maize, soybeans, and sorghum, so the higher output figures weren't surprising. Since more people are moving into the middle class and expecting meat to be a staple food, demand for these grains has increased globally. Each grain's output increased between 2020 and 2021 and is used to make animal feed.

Many grains can be readily transported over large distances, stored for extended periods, processed into flour, oil, and gas, and consumed by animals and people.

A small amount of grain in the US is processed into ethanol, while the majority is utilized as animal feed. Humans consume the lowest amount. The health and morality of feeding grain to animals like cows, goats, and sheep, who are naturally better suited to eating grass, has recently been the subject of discussion. Some claim that this approach negatively impacts the quality of the meat and the health of the animal and the customer, despite being more cost-effective than grass feeding.

The number of grains used to make ethanol has dramatically grown in recent years. Since the year 2000, ethanol output has increased greatly globally. A feedstock, commonly sugar cane or maize cobs, is fermented to produce ethanol, a semi-renewable energy source. It may be used as motor vehicle fuel when combined with gasoline. Compared to regular gasoline, this hybrid motor fuel releases fewer pollutants.

Wheat- A considerable increase in global output is predicted, with greater crops in India, Russia, the EU, and Ukraine. Global commerce has increased because of increased exports from Russia, the EU, India, and Ukraine, due to a larger supply. Due to increased demand from China and the impact of severe rains on some developing countries, imports are expected to increase. As a result of rising feed and residual use in China, Russia, and India, which more than makes up for falling food, seed, and industrial (FSI) usage in Syria, the world's consumption is expected to rise. The season-average farm price in the United States is predicted to fall 10 cents to $7.20 a bushel.

Except for a decrease for Hard Red Winter, U.S. quotations have been generally stable since the October WASDE (HRW). Due to the weak export sales thus far and the fierce competition from Russia and Canada in the Western Hemisphere markets, HRW prices fell from $16 per ton to $289. Soft Red Winter (SRW) increased in price per ton to $256 due to robust Chinese demand. Due to increased competition, SRW sales to China have more than doubled from the same time last year. Hard Red Spring (HRS) and Soft White Wheat (SWW) remained mostly unaltered.

Rice- With a greater expected harvest for India, offsetting lesser projections for Thailand and Cambodia, global rice output is almost unchanged. With rises for India and the Philippines, global consumption is up. Higher imports are anticipated, especially for Kenya and the Philippines. The expected increase in global stockpiles is attributed to the forecast of a sharp rise in India's carryover stocks starting in 2022–2023.

U.S. export quotations have stayed at $760/ton over the previous month, while Uruguayan quotes increased $10 to $760/ton due to high demand and limited supply. These rivals' quotes are identical for the first time in more than two years. Vietnamese quotations increased from $60 to $676/ton due to increasing demand from Africa, Indonesia, and the Philippines, but they are still far more expensive than those of other Asian suppliers. Thai prices decreased by $32 to $563 per ton as the market saw the arrival of fresh crop harvest. Pakistani quotations increased marginally to $555/ton as robust demand brought on by India's ongoing export restrictions countered harvest constraints. White rice from India is not accessible for export since an export embargo was implemented on July 20.

Corn The prognosis for Zambia and Ukraine is for increased grain output worldwide. Global commerce is anticipated to improve as growth in Ukraine and Brazil more than offsets declining exports from Argentina. On the strength of the European Union's increased demand, an increase in global imports is predicted. The U.S. season-average farm price is down 10 cents per bushel to $4.85.

All significant exporters have seen a drop in bids since the October WASDE. US bids were $211 per ton, $20 less than the previous month. Bids are becoming softer due to seasonal pressure from the continuing harvest and decreased logistical costs. Bids from Brazil were $220/ton, a little less than they were the month before. The constraints faced by inland logistics are counteracting the downward pressure from the huge supply, therefore stabilizing prices. Compared to last month, Argentine bids were down $46 to $212 per ton. The push from other exporters to compete is causing prices to drop dramatically.

Since July 21, there have been no published proposals from Ukraine.