Food prices are a big concern for consumers in today’s world. Rising global food prices affect the lower-income group the most. Food is becoming more expensive due to weather shocks, export bans, inflation, high oil prices, a rise in the cost of biofuels, speculation, slow growth in farm yields, and the expensive seeds essential for growing crops providing food to the consumers.

Prices of corn and soybeans are reaching new highs daily, but this is not resulting in any profits for the producers because they suffer from the excessive cost of producing these commodities.

Corn is the largest feed grain domestically and globally. Corn accounts for over 85% of total U.S. feed grain production. The United States is the largest producer of corn in the world, averaging 210 million metric tons from 1990-96, representing about 40% of global production.

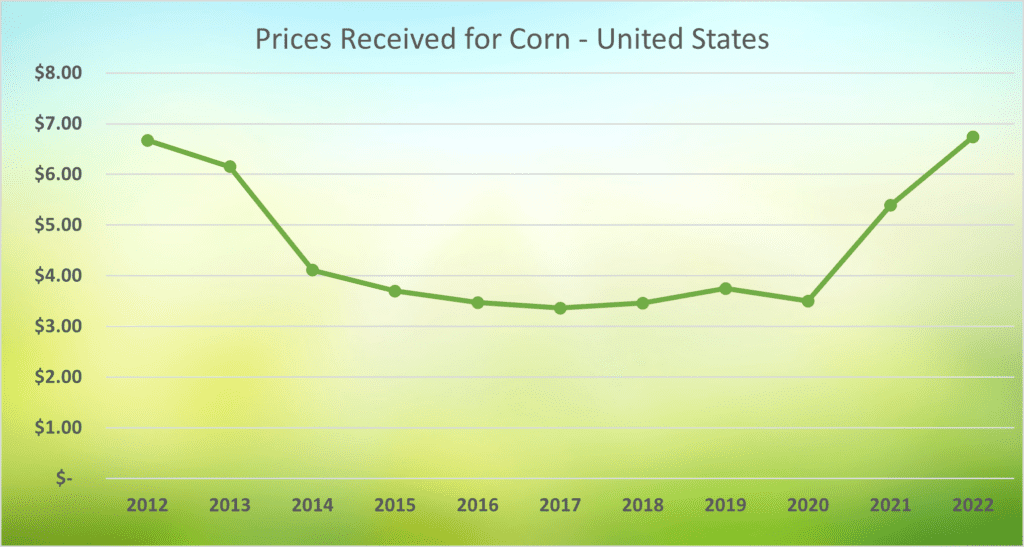

The current price of corn is $6.8000 per bushel which is getting back on track now as the result of an agreement between Russia and Ukraine. This allows Ukrainian grains to be shipped through the Black Sea. However, the current price of the commodity is much higher than the opening price of this year. The corn price is driven by supply and demand factors, largely dominated by U.S. agricultural policies according to the U.S. Department of Agriculture (USDA).

Currently, the low supply of seeds is being caused by poor weather conditions in North Dakota, which has reduced the supply since last year. As per the Global Trade Article, North Dakota contributes 85% of total American rape seed output which is brutally affected by bad weather conditions in North Dakota. The ongoing drought conditions, heat, and excess humidity coupled with rainfall deficit are also intense factors that contribute to the rising seed prices as the quality of the soil continues to be poor for harvesting.

Demand is comparatively high due to the industrial use of corn in producing starch, ethanol, and alcoholic beverages. The use of corn as food consisting of cereals, and corn sweeteners has grown sharply over the past 20 years. Demand for corn-based cereals, snack foods, and baked goods is expected to increase further with the growth of the population.

The United States is a major wheat-producing country. Wheat ranks third among U.S. field crops in planted acreage, production, and gross farm receipts — behind corn and soybeans. Wheat is used for making a variety of food such as bread, pasta, cake, and flour. Wheat is unique because it is the only cereal grain with sufficient gluten to produce bread without the requirement of mixing it with another grain. Due to this fact, wheat is the most demanded cereal.

Source

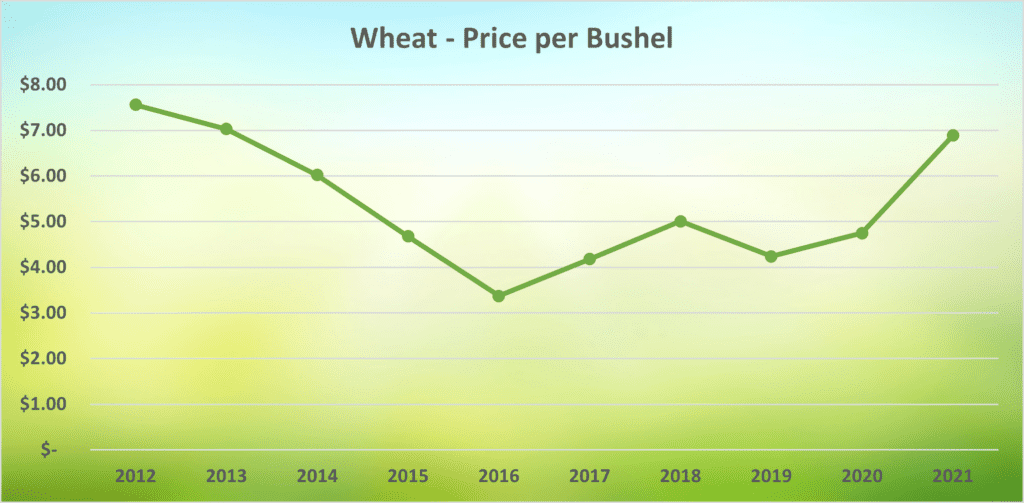

The monthly price of wheat (hard red winter) in the United States reached an all-time high in May

2022, costing over 520 $U. S. per metric ton. The average wheat prices increased by 165% between May 2021 and May 2022, with the bulk of the increase noticed after February 2022.

The seeds market in the U.S. has the potential to grow by USD 10 billion during 2021-2025, and the market’s growth momentum will accelerate at a CAGR of 8.71%. The seeds market in the US is fragmented. The vendors are deploying organic and inorganic growth strategies to compete in the market and make the most of the opportunities. The vendors are trying to recover from the post-COVID-19 impact, Russia- Ukraine War, and adverse weather conditions.

According to the Forecast by the Food and Agriculture Organization of the United States (FAO) for 2022/23, world cereal utilization has been lowered by 5.1 million tonnes since July to 2792 million tonnes, representing a marginal decline of 0.1% (2.8 million tonnes) from the 2021/22 level. World trade in cereals in 2022/23 is forecast at 469.6 million tonnes, up by 2.0 million tonnes since the July report but still 1.9% below the 2021/22 level. At 191.3 million tonnes, the forecast for world wheat trade in 2022/23 (July/June) remains nearly unchanged since July and still points to a 1.8% decline from the 2021/22 (July/June) level. Greater wheat export prospects for Canada and the Russian Federation, boosted by higher production forecasts, are balanced by lower expected shipments from the European Union, as a result of lower production prospects, and India, where the country’s efforts to control rising domestic prices through wheat export restrictions, are seen tempering exports. However, increased maize production expectations in Ukraine lifted FAO’s forecast for Ukrainian maize exports in 2022/23 by 2.0 million tonnes to 17.0 million tonnes. The forecast for global maize trade in 2022/23 (July/June) is now at par with the 2021/22 estimated level of 181 million tonnes. Nonetheless, as per the forecast, the world trade in coarse grains in 2022/23 (July/June) is expected to fall by 2.6% from 2021/22 to 223 million tonnes, because of expected declines in the global trade of barley and sorghum. In the case of barley, the decline is mostly due to foreseen reduction in demand from China and Turkey, and smaller shipments from Australia and Ukraine, whereas in the case of sorghum, the decline stems almost exclusively from expectations of tighter export availabilities in the United States of America and smaller imports by China. International trade in rice is seen to reach 54.4 million tonnes in 2022 (January/December) and 55.0 million tonnes in 2023. India is predicted to remain the largest rice exporter in the world, shipping over 20.0 million tonnes annually.

The rising price of corn, wheat, and other food commodities is contributing to the highest inflation rates the U.S. has seen since the 1980s and it may remain the same in 2023 too. The government needs to ensure rational utilization of production resources and recommend minimum support prices for the primary resources used in agricultural practices. This way the total cost of production will not be affected, and we will see stability in inflation which will also provide additional subsidies to the farmers.